Ahh ok I see what you (and @davidlkl) originally meant now.

The answer is not going to be very satisfying I’m afraid: these are small measurement errors.

In reality when we have to construct the quantiles, it’s not always exactly equal and we have to allow the algorithm some leeway to make things approximately equal. When the market share is very low, when we are contructing these buckets, that error becomes relatively large. Hence the issue you observe.

I’m attaching another feedback with a average marketshare of ~0.05 so you can see that the numbers become closer when the buckets are constructed using more inputs.

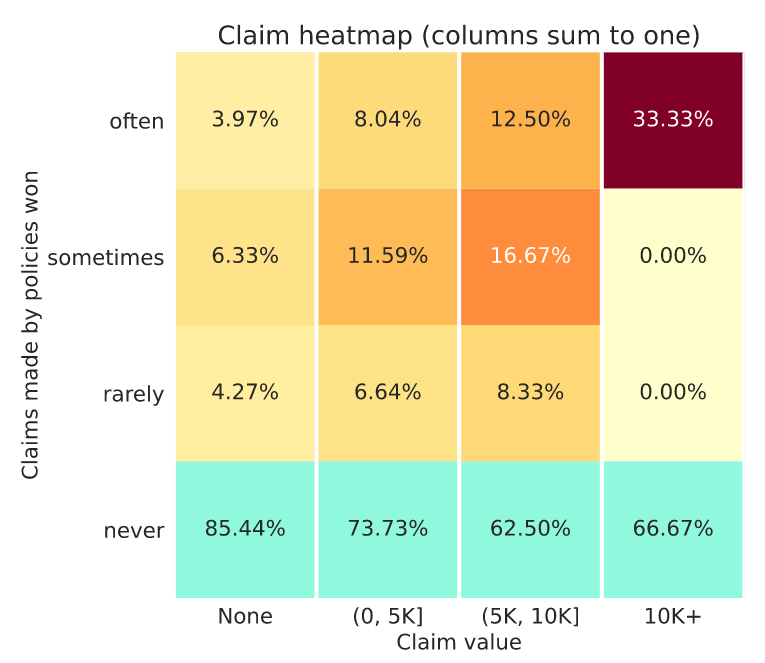

Here assuming claim frequency of each category being 10% of the last.

I’m not sure what others think but I’d say that the ideal plot* could look something like this:

Of course you could say that if you price things properly you want to get some of the claims and still make money, but this is just one version of what a good plot could look like.

If I assume that’s your feedback from week 9 submission then I’d conclude that it’s not ideal.

In many ways it’s similar to my week 8 submission when I had a similar looking chart, a similar high market share and a low leaderboard position. The difference is my week 8 RMSE model was 500.1 ish and your week 9 is 499.46 ish.

Now you’d hope that a model with a much lower RMSE should be better at differentiating risk. If that was the case though you’d expect to write a smaller market share of the the policies with higher actual claims. Your chart though doesn’t show such behaviour. That may be because your good performance on the public RMSE leaderboard is not generalising to the unseen policies in the profit leaderboard. This could be a result of placing too much emphasis on RMSE leaderboard feedback and not enough on good local cross validation results. It can lead to unwittingly overfitting to the RMSE leaderboard at the expense of a good fit to unseen data.

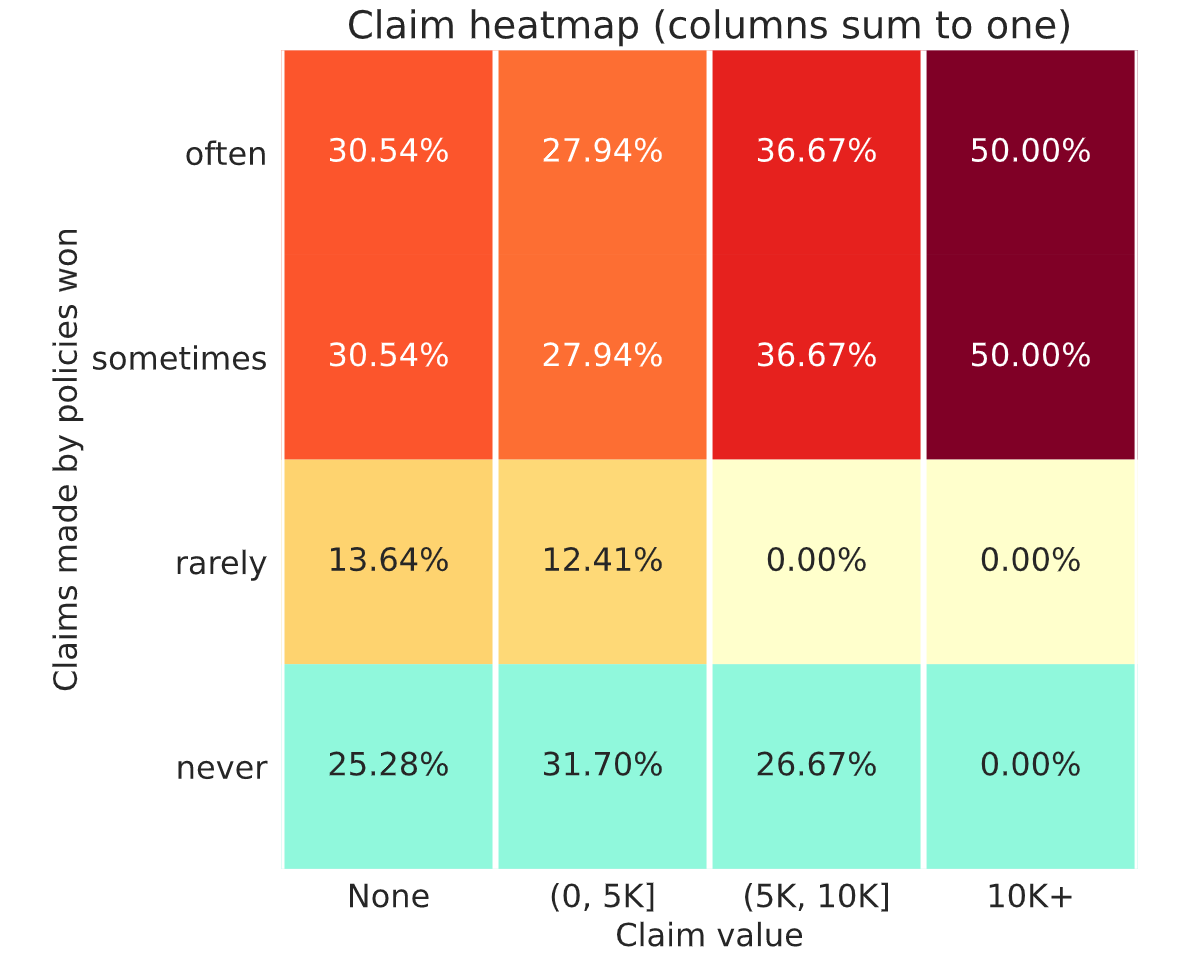

Now I think I have a similar issue, ie a poor fitting model as my week 8 and week 9 charts are less that ideal… (I’d rather have a chart like @davidlkl but with greater market share). But the cause of my issue is that in seeking not to overfit too much I haven’t fit well enough relative to others.

Another point to investigate is your market share. A 30% market share, suggests your profit margin is set lower than competitors. In a pool of 10 people a 10% market share would be a a reasonable target to go for.

The only difference between my week 8 and week 9 submission was that I increased my rates by a fixed single digit percentage. I’ve learnt that I perhaps increased rates too much as my market share has fallen further than I’d like.

So for my final submission I’ll be refining my model and making a minor tweak to my profit margin. (And no doubt subsequently regretting doing so as I see my profit leaderboard position plummet!)

I’ve been giving this a lot of thought… that it’s now given me a headache. So, I’ve been hung up on how there isn’t a strong correlation between RMSE and profit in the leaderboards (thanks @michael_bordeleau for simulating the profit correlations with other metrics) . Not that I expected a perfect correlation, but I did initially expect that there would be a much stronger correlation than what we’re seeing. Thinking about this more, I think what this line of thinking is missing is that in a sample against 9 other models, you just need one better model in the 9 competitors to get adversely selected against.

There are around 20 models in the top 10 percentile deemed “competitive” that all models are competing against. Let’s say there’s 1 super good model and the rest are all baseline models. The chances of your model being put up against the super good model is (19 choose 8) / (20 choose 9) = 45%.

So even if there’s just 1 model that’s better than yours in the top 10 percentile, you’re going to be against it almost half the time. In those situations, your model’s profit is going to be if there are pockets of profitable business that the really good model is not capturing and yours is. Since in this hypothetical situation, the super good model is better than yours, you wouldn’t be able to tell where those pockets are.

If this thinking is correct, maybe RMSE isn’t the best metric to use, but having a really good model still matters quite a bit.

The other variable in the profit leaderboard is how much profit load competitors are tacking onto their pricing strategy. Based on the discussions, it seems that many people are increasing their profit loads (we also see more participants with profit in the more recent weeks). So there’s also a guessing component of what others are doing because if everyone else increases their loads, then you probably need to too. But are they? And if so, by how much? I wish we could get “industry feedback” every week. That would be interesting to see on average how much loads competitors are charging. I wouldn’t add this feature this late into the competition, but maybe for the second round .

Not knowing how your price compares to the market definitely makes this challenge more difficult than real life insurance, where you can just ring your competitor, or visit their website to get a quote.

The problem is that the industry load (which is essentially an average) will not help. At least for me, I do different load for different segment. You can’t tell which segment I am going after even if I tell you my portfolio average.